By Pete Pennicott | October 26, 2022

By Pete Pennicott | October 26, 2022

Last night the Treasurer, Jim Chalmers, released the Government’s October 2022-23 Budget.

The Budget featured a range of proposed measures including superannuation, tax, Social Security and Aged Care changes.

Our summary of the key changes which may impact your financial planning are outlined below. As always if you have any questions please email me or book a chat.

Downsizer contributions allow eligible individuals to contribute up to $300,000 to superannuation upon selling an eligible main residence. From 1 July 2018 until 30 June 2022, the minimum qualifying age to be eligible to make a downsizer contribution was age 65. From 1 July 2022, the minimum qualifying age was reduced to age 60.

On 3 August 2022, the Government introduced Treasury Laws Amendment (2022 Measures No. 2) Bill 2022 into Parliament, which if legislated, will ensure that the minimum qualifying age for downsizer contributions will be reduced to age 55.

Notes:

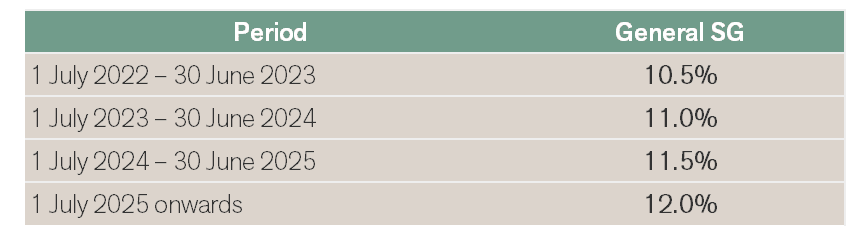

Currently, Superannuation Guarantee (SG) is 10.5%. It is legislated to increase by 0.5% at the start of each financial year from here on in until it reaches 12% on 1 July 2025.

There is no change to the legislated increase of SG.

There was no announcement concerning extending the halving of the SIS minimums beyond the 2022-23 financial year in relation to eligible income streams such as account-based pensions and market linked pensions.

In recent Federal Budgets, there have been a number of announcements relating to superannuation. The Government took the opportunity in the to provide clarity on the progress of specific unlegislated proposals.

In the 2018-19 Federal Budget, the previous Government had proposed that from 1 July 2019, the annual audit requirement will be changed to a three-yearly requirement for SMSFs with a history of good record-keeping and compliance. This measure was proposed at the time to reduce red tape for SMSF trustees that have a history of three consecutive years of clear audit reports and that have lodged the fund’s annual returns in a timely manner.

The Government has confirmed that this measure will not go ahead.

In the 2021-22 Federal Budget, the previous Government had proposed to allow the relaxation of residency requirements for SMSFs and Small APRA Funds (SAFs) by extending the central management and control test safe harbour rule from two to five years for SMSFs and removing the active member test for both SMSFs and SAFs. It was expected for this measure to take effect from 1 July 2022.

The Government has reaffirmed its support for this measure with the effective date to be delayed to the income year commencing on or after the date of Royal Assent of the enabling legislation.

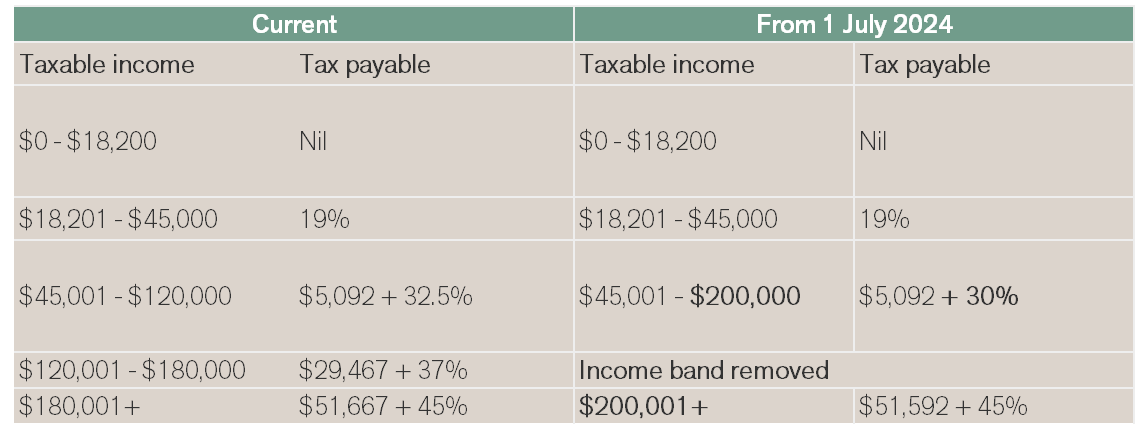

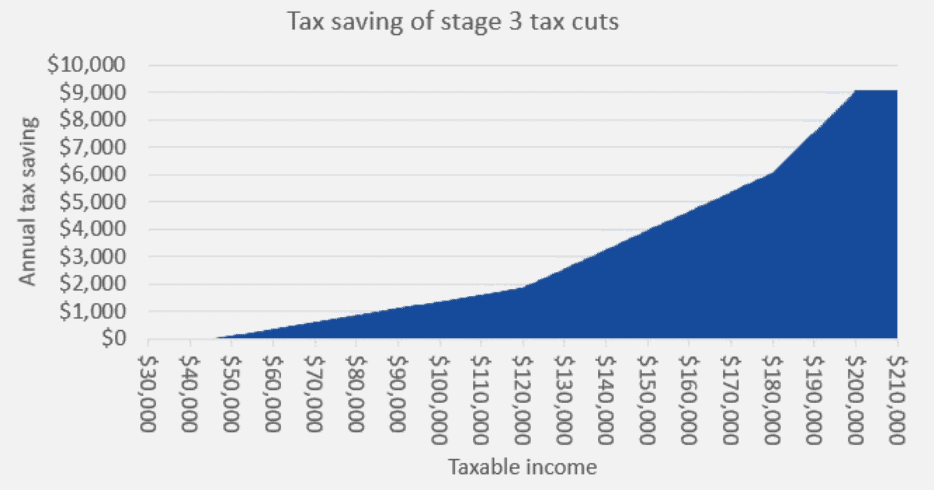

Despite the ongoing debate about deferring or cancelling the stage 3 tax cuts, the measure will go ahead in accordance with the legislated timetable from 1 July 2024. The stage 3 tax cuts that were introduced as part of the previous Government’s personal income tax reform, will remove the 37% income band and increase the higher threshold in the 45% income band from $180,000 to $200,000. The applicable rate on the 32.5% income band will also reduce to 30%.

Source: Colonial First State

The Government will improve the integrity of the tax system by aligning the tax treatment of off-market share buy-backs undertaken by listed public companies with the treatment of on-market share buy-backs.

Note:

This measure will apply from the announcement on Budget night (7:30 pm AEDT, 25 October 2022).

The Government will cut taxes on electric cars so that they will be affordable for more Australians.

From 1 July 2022, the measure will exempt battery, hydrogen fuel cell and plug-in hybrid electric cars from fringe benefits tax and import tariffs if they have a first retail price below the luxury car tax threshold for fuel-efficient cars ($84,916 in 2022‑23).

Note:

The Government recommitted to freezing the current deeming rates until 30 June 2024. The deeming thresholds will continue to be indexed on 1 July each year.

Principal home sale proceeds all at lower rate for exemption period. This rate would also not impact deeming threshold for other financial assets.

The current deeming rates and thresholds are as follows:

The Government recommitted to increasing the income thresholds for the Commonwealth Seniors Health Card from $61,284 to $90,000 for singles, from $98,054 to $144,000 for couples and from $122,568 to $180,000 for couples separated by illness, respite care, or prison.

Notes:

The Government recommitted to extending the exemption period for proceeds from selling the principal home to purchase or build another home. Specifically:

Notes:

The Government is providing an immediate one-off increase to an eligible pensioner’s Work Bonus income bank of $4,000 during 2022-23. This will increase the maximum unused income bank to $11,800 from $7,800 and allow pensioners to work more hours without affecting their pension.

These changes will not affect the existing application of the $300 fortnightly Work Bonus. Instead, the changes will provide an immediate $4,000 increase to the income bank of all eligible pensioners. This will allow eligible pensioners to have an extra $4,000 of income from work immediately disregarded from the income test rather than having to accumulate a balance over time.

Notes:

The Government will provide funding to decrease the general patient co-payment for treatments on the Pharmaceutical Benefits Scheme (PBS) from $42.50 to $30.00 from 1 January 2023. The existing Medicare Safety Net provisions and all prescriptions that currently count towards a patient’s Safety Net will continue to do so.

Changes are also being made to ensure Closing the Gap patients will not need to pay any more to reach their Safety Net. A script with a Commonwealth price at or above the co-payment amount will have the script count toward the PBS Safety Net at a fixed value of $42.50, rather than at the reduced $30.00 co-payment. This will remain until the general patient co-payment is more than $42.50 in the future through indexation.

The Government will provide $4.7 billion over 4 years from 2022–23 (and $1.7 billion per year ongoing) to deliver cheaper child care, easing the cost of living for families and reducing barriers to greater workforce participation. This includes $4.6 billion over 4 years from 2022–23 to:

The Government will introduce reforms from 1 July 2023 to make the Paid Parental Leave Scheme flexible for families so that either parent is able to claim the payment and both birth parents and non-birth parents are allowed to receive the payment if they meet the eligibility criteria. Parents will also be able to claim weeks of the payment concurrently so they can take leave at the same time.

Both parents will be able to share the leave entitlement, with a proportion maintained on a “use it or lose it” basis, to encourage and facilitate both parents to access the scheme and to share the caring responsibilities more equally. Sole parents will be able to access the full 26 weeks.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).